Finally — Time for Brand Reckoning at Stellantis?

Stellantis today posted its first-ever annual loss after booking substantial write-downs amid a major strategic shift. Full-year 2025 net loss was 22.3 billion euros ($26.3 billion USD), compared to full-year profit of 5.5 billion euros a year ago.

The net loss was impacted by 25.4 billion euros in write-downs, Stellantis said, as the company sharply scales back its electric vehicle strategy.

Stellantis CEO Antonio Filosa said in a statement;

“Our 2025 full year results reflect the cost of over-estimating the pace of the energy transition and of the need to reset our business around our customers’ freedom to choose from the full range of electric, hybrid and internal combustion technologies. In 2026 our focus will be on continuing to close the execution gaps of the past, adding further momentum to our return to profitable growth.”

Stellantis said it had suspended its dividend for 2026, as it had previously flagged, and issued up to 5 billion euros of hybrid bonds. It also reiterated its 2026 forecasts, including a mid-single-digit percentage increase in net revenues and a low-single-digit adjusted operating margin.

Stellantis said it expects positive industrial free cash flow in 2027.

Over the second half of 2025, Stellantis said it delivered a “solid” performance, noting consolidated shipments came in at 2.8 million units, with North America posting the strongest contribution.

Net revenues rose 10% to 79.25 billion euros through the latter half of 2025 when compared to the same period a year ago.

These results reflect the initial impact of improved operational efficiencies, disciplined commercial strategies and the strength of the firm’s global brand portfolio, Stellantis said.

Stellantis does not break down its financial results by individual brand — the company reports earnings by geographic segment (North America, Enlarged Europe, South America, Middle East & Africa, etc.),

Stellantis FY 2025 — Results by Geographical Segment

North America Net revenues came in at €60.96 billion (vs. €63.45 billion in 2024, down ~4%), with an adjusted operating loss of €1.89 billion — an AOI margin of -3.1%, a dramatic swing from +4.2% in 2024. Shipments were up 3%, driven primarily by Ram LD trucks, Jeep Wrangler/Gladiator, and Chrysler Pacifica. The loss was driven by unfavorable mix, U.S. tariffs, a change in contractual warranty estimates, and higher incentive spend.

Enlarged Europe Net revenues were €57.77 billion (vs. €59.01 billion in 2024, down ~2%), with an adjusted operating loss of €651 million — an AOI margin of -1.1%, down from +4.1% in 2024. Shipments fell 3%, hurt by lower volumes of legacy Peugeot, Opel, and Fiat models, partially offset by the new Opel/Vauxhall Frontera and Fiat Grande Panda.

South America Net revenues were €16.20 billion (vs. €15.86 billion in 2024, up ~2%), with adjusted operating income of €1.96 billion — an AOI margin of 12.1%, down from 14.3% in 2024. Shipments rose 10%, driven by higher volumes in Argentina, Brazil, and Chile, though the Brazilian Real and Argentine Peso devaluations weighed on profitability.

Middle East & Africa Net revenues were €9.71 billion (vs. €10.10 billion in 2024, down ~4%), with adjusted operating income of €1.43 billion — an AOI margin of 14.7%, down from 18.8% in 2024. Consolidated shipments rose 7%, mainly driven by Türkiye, though negative foreign exchange effects from the Turkish Lira weighed on both revenues and profits.

Summary Table (FY 2025):

| Segment | Net Revenues (€bn) | AOI (€bn) | AOI Margin |

|---|---|---|---|

| North America | 61.0 | (1.9) | -3.1% |

| Enlarged Europe | 57.8 | (0.7) | -1.1% |

| South America | 16.2 | +2.0 | 12.1% |

| Middle East & Africa | 9.7 | +1.4 | +14.7% |

| Group Total | 153.5 | (0.8) | -0.5% |

| Segment | Net Revenues (€bn) | AOI (€bn) | AOI Margin |

|---|---|---|---|

| North America | 61.0 | (1.9) | -3.1% |

| Enlarged Europe | 57.8 | (0.7) | -1.1% |

| South America | 16.2 | +2.0 | 12.1% |

| Middle East & Africa | 9.7 | +1.4 | +14.7% |

| Group Total | 153.5 | (0.8) | -0.5% |

South America and Middle East & Africa were the only two regions to remain profitable in 2025. North America and Enlarged Europe — historically the most important segments — both swung to losses, largely driven by the sweeping EV-related write-downs and strategic reset charges.

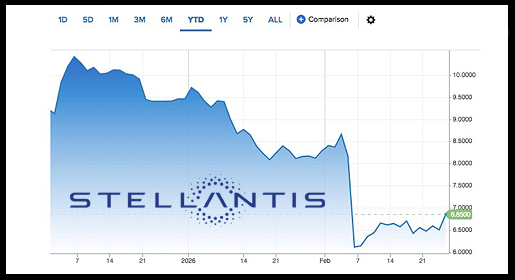

Milan-listed shares of Stellantis rose 0.4% on the news. The stock is down more than 31% so far this year.

The Core Problem

Managing 14 brands is a heavy load, and keeping all of them profitable while avoiding overlaps and wasted resources has been a structural challenge Stellantis has faced since its creation in 2021 when FCA and PSA merged. Even at that time, many analysts questioned the sustainability of such a broad portfolio.

A Formal Review Is Now Underway

Antonio Filosa is formally assessing the performance of all 14 Stellantis brands in global markets, and eliminating underperforming brands is explicitly on the table. According to Reuters, European brands would likely be the primary targets for any cuts. Year-end U.S. sales are expected to play a role in assessing the future viability of some brands, as Filosa works on a long-term strategy to reassure investors that Stellantis is still structurally sound. The company’s so-called “emergency room” review could reshuffle which brands grow, merge, or fade away.

Brands Most at Risk

The brands most frequently cited by analysts and industry observers include:

- Alfa Romeo — Alfa Romeo is growing in percentage terms but remains a tiny niche brand by volume, heavily dependent on a single model. In its home market of Italy, Alfa Romeo ranked only 20th nationally in 2025 — behind Suzuki, Nissan, Skoda, MG, and Kia — despite being up 23% on 2024. In the USA for 2025, Alfa Romeo sold 5,652 vehicles, which was a decrease of 36% compared to the previous year.

- DS Automobiles — DS has struggled to fully capitalize on its premium positioning, and is also viewed as vulnerable.

- Citroën — Citroën is positioned at the value-conscious, mass-market end of the spectrum — catering to buyers looking for practical, affordable yet avant-garde vehicles. This places it alongside Fiat and Opel in the more accessible tier, sitting well below the premium DS Automobiles. Investors have speculated that Citroën may inherit DS Automobiles as the “luxury cache” of DS Automobiles has not been attained and DS models could be sold by Citroën with the reputation built and still recognized by their iconic models that were shifted to DS Automobiles.

- Dodge — Dodge had a much tougher year overall, though it recovered sharply by year-end. Full-year shipments fell 28% to 101,927 units, with the aging Durango doing the heavy lifting — jumping 37% to 81,168 vehicles, its best sales year since 2005. The brand was effectively a one-model show for most of the year, as the transition away from the old Challenger/Charger lineup left a major gap.

- Fiat – The most striking fact about Fiat globally is where its volume actually comes from. Between January and September 2025, Fiat sold just over 661,000 cars worldwide — and Brazil alone accounted for 384,639 of those registrations, more than three times Fiat’s sales in Italy over the same period. In the USA in 2025, Fiat sold 1,321 vehicles, which was a decrease of 14% compared to the previous year.

- Jeep — Jeep is Stellantis’ most important single global brand, and its 2025 performance was ultimately a recovery story — painful in the first half, but gaining real momentum by year-end.

- Lancia — Analysts have hypothesized that Lancia may be a target for a sale given its smaller profile. The history of Lancia under Sergio Marchionne — surviving for years with a single model sold only in Italy — serves as a cautionary reference point.

- Chrysler — Chrysler is a huge name, but the brand is down to just the Pacifica and Voyager minivans. However, closing a brand in America is complicated because of the complex relationship between automakers and their dealers, and a century of brand equity is a lot to give up — reinvigorating Chrysler might be a better bet than ending it.

- Maserati — Maserati continues to face very low volumes and an unclear strategic direction, making its situation particularly delicate. Rumours have been swirling for some time that Alfa Romeo and Maserati might be complied into one brand.

- Opel — Opel has also entered the conversation, though not because of weak sales. The most widely discussed scenario involves repositioning it as a European testbed for more affordable technologies developed in cooperation with Stellantis’ Chinese Leapmotor affiliation.

- Peugeot — Peugeot is arguably the strongest of Stellantis’ European brands right now — it has genuine volume, competitive models, EV momentum, and strong brand recognition. It is clearly not at risk of elimination and, along with Fiat and Opel, forms the core of Stellantis’ European mass-market strategy. The big structural challenge, as noted earlier, is that Peugeot still competes heavily for the same customers as Citroën and Opel within the same corporate family.

- RAM – Ram was a genuine bright spot and ended 2025 on a high. December 2025 was Ram’s best December for total sales since 2021, up 6% year over year. Ram 1500 sales jumped 23% in Q4, and across the full lineup retail sales improved in every major category — light-duty trucks rose 27%, heavy-duty models increased 7%, chassis cab sales climbed 11%, and ProMaster vans gained 9%.

- Vauxhall — The Vauxhall Corsa was crowned the UK’s best-selling super-mini of 2025, capturing a 13.9% share of the B-hatch segment — up 3 percentage points year-over-year — with 35,967 units sold. However, the commercial vehicle collapse and EV under-performance are real concerns.

The Bottom Line

2026 is shaping up to be a turning point. The decisions made will shape not only the fate of several historic brands, but also Stellantis’ ability to remain competitive in an increasingly crowded market under pressure from Chinese rivals and ever-stricter European regulations.

For some time now, rumours have been circulating about the future of our DS Automobiles and Citroën within Stellantis. The subject of a possible return of DS Automobiles as a simple premium entity of Citroën has been somewhat fuelled by the arrival of Citroën in Formula E, in which DS Automobiles has been competing since the beginning of the championship.

The reality is that since its inception, Stellantis has led a particularly vast and diverse portfolio of brands—fifteen, if we include the recent integration of Leapmotor. The objective was to create synergies while allowing each brand to express its identity. The need to achieve substantial cost savings has become a priority and financial results have indicated for some time that the elimination of certain brands deemed less profitable are a course that executive management must undertake. DS Automobiles is often mentioned, with the scenario of reintegration, rather that elimination, into the Citroën range while still being a premium offering above the current C5 Aircross.

After investing so much to create a distinct identity, a distinct distribution network, and a premium brand image, this strategy would allow for substantial economies of scale in key areas such as marketing, communications, and support functions while bringing the lineage of DS luxury and innovation back into Citroën. It would give DS Automobiles the time it needs to continue its development and reach maturity, in a broader and integrated fashion within Citroen, that could be marketed to the benefit of both.

Stellantis has an Investor Day scheduled for May 21, 2026 in Auburn Hills, Michigan, where more clarity on brand strategy is expected.